Market Report Q1/2026 – The End of the Old Order – Commodities Are Part of the Security Architecture

The price question becomes an access question

With “Readiness 2030”, the EU plans to mobilize up to €800 billion for defense and military capabilities.

Geopolitical tensions in recent months have changed perceptions of reliability within existing alliances. In particular, increasingly hard-to-predict US policy is driving a growing need in Europe for strategic autonomy. The EU is responding not only with higher defense spending, but also with a clear focus on securing critical commodities. New partnerships, alternative sources of supply, and domestic capacities are moving to the forefront—as the foundation for industrial and security-policy capability to act.

Geopolitics and security of supply

Venezuela – commodities, currencies, and geopolitical interests

In January 2026, the geopolitical situation reached a new level of escalation: in a rapid military operation, the United States attacked Venezuela and abducted President Nicolás Maduro. The attack marks more than a regional conflict. It marks the beginning of a quarter in which it once again becomes clear how closely commodities, payment flows, and geopolitical interests are intertwined. In this context, some economists and geopolitical analysts point to recurring patterns: whenever commodity-rich states attempt to move away from the dollar as the leading currency in oil trading or establish alternative settlement systems, tensions arise—often accompanied by political or military conflicts.

Thus, in 2000 Iraq announced that it would trade oil in euros in the future. Libya also pursued considerations from 2009 onward regarding a gold-backed African currency. In recent years, Venezuela began increasingly settling oil in alternative currencies, while Russia and Iran use alternative payment systems, and discussions in Saudi Arabia about settlements outside the dollar are also gaining importance.

At the same time, the strategic value of Venezuelan resources remains central. Venezuela has the world’s largest proven oil reserves, and observers see economic interests—particularly access to energy—as an important factor in the background of the conflict.

Against this backdrop, some observers interpret the escalation in 2026 not only as an isolated event, but as part of a broader geopolitical field of tension. At its core is the question of what role the US dollar will play in global commodity trade going forward—and which interests are tied to its stability.

For a more in-depth analysis of these connections, please refer to our article:

The End of the Petrodollar – Why Commodities Are Now the True Currency?

New partnerships – access to raw materials is being organized strategically

Despite ongoing resistance from agriculture and individual member states, the European Union is continuing to push the Mercosur agreement forward. What long appeared to be a classic free-trade project is now taking on a new strategic dimension.

For Europe, it is increasingly no longer just about market access, but about secure access to critical commodities. Countries such as Brazil and Argentina have significant deposits of lithium, niobium, graphite, and rare earths—resources that are indispensable for e-mobility, energy infrastructure, and defense technologies.

The geopolitical context further intensifies this development. Export controls, trade conflicts, and China’s strong market position in refining make it clear how vulnerable existing supply chains are. In this environment, trade agreements take on a new function: they become instruments for securing commodities.

At the same time, Europe is also intensifying bilateral partnerships with resource-rich countries. Talks with states such as Kazakhstan show that, alongside major trade agreements, targeted cooperation, technology transfer, and direct supply relationships are increasingly being established.

The focus is therefore shifting more and more—away from pure trade and toward securing access. It is no longer the cheapest supplier that decides, but reliable access to resources.

You can find an article on a planned economic cooperation with Kazakhstan here.

Strategic reserves and government intervention are changing the market

Critical commodities are increasingly moving to the center of government strategies. What long seemed like a market issue is now being deliberately steered politically.

In the United States, this shift is becoming particularly clear. With “Project Vault”, the government has launched an initiative worth around $12 billion to build strategic reserves of critical metals. The aim is to reduce dependence on external supply chains and ensure targeted supply to industry in a crisis—comparable to the Strategic Petroleum Reserve in the energy sector.

In addition, a bipartisan bill has been introduced that provides a further $2.5 billion for building state-coordinated commodities reserves. The state is therefore no longer acting only as a regulator, but is becoming an active market participant itself.

Australia is pursuing a similar strategy. The government is investing A$1.2 billion in a national commodities reserve that specifically secures materials such as gallium, antimony, and rare earths—commodities that are indispensable for semiconductors, defense systems, and energy technologies. What stands out is not only the scale of the programs, but their nature: through strategic reserves, offtake guarantees, and state-coordinated investments, the aim is to stabilize supply and secure access in a crisis.

This development also became clear at the 2026 Munich Security Conference. Under the title “Under Destruction”, leading politicians and experts described a world order in upheaval, in which security can no longer be taken for granted. Europe is responding with greater autonomy, new alliances, and the targeted expansion of its industrial and military capabilities.

Commodities are therefore no longer traded exclusively—they are secured strategically. Security of supply is evolving from an economic issue into a central component of national security architecture.

The Noble Group was also live on site at the Security Conference.

Energy, escalation, and control – who controls global raw material flows

The escalation in the conflict between the United States, Israel, and Iran brings one of the most sensitive bottlenecks in global energy supply into focus: the Strait of Hormuz. Around one fifth of the world’s traded oil passes through this strait every day—much of it destined for Asia, especially China and India.

Current tensions show how quickly geopolitical conflicts become real supply risks. Even short-term disruptions lead to rising energy prices, interrupt supply chains, and increase uncertainty in the markets. Energy thus once again becomes a geopolitical lever.

At the same time, the situation reveals a structural weakness of the West. Strategic decisions are increasingly made unilaterally, while the economic consequences are distributed globally. For Europe, this raises the question of how reliable existing partnerships still are in an environment of growing geopolitical tensions.

At the same time, another actor is increasingly moving to the forefront: China. While Western states react to crises in the short term, Beijing is pursuing a long-term strategy. Control over refining, strategic reserves, and industrial capacities gives China a position from which it can significantly influence global developments.

The crisis in the Persian Gulf makes it clear that raw material security has multiple dimensions: access, political control, and physical transport routes. But it also shows that the ability to manage these factors is unevenly distributed.

In a world in which energy flows are disrupted, supply chains are politicized, and alliances are reassessed, the balance of power is shifting. No longer do military strength or economic size alone decide—but rather control over the critical resources and systems on which both are built.

You can read here how China’s strategy fundamentally differs from the West’s.

Control without new measures

In the first quarter of 2026, China did not introduce any new export controls. However, the existing restrictions on critical metals such as gallium and germanium remained fully in force—and are increasingly taking effect.

Instead of further tightening, a different dynamic is emerging: the existing instruments are sufficient to steer global supply chains in a targeted manner. Export licenses are granted selectively, trade flows shift, and certain buyer countries receive temporary preferential access.

At the same time, a differentiated picture is emerging for rare earths. While export volumes for certain metals have increased, regulatory requirements remain high. For many shipments, the precise end use must be disclosed—an intervention that goes far beyond classic trade controls.

This creates a structural problem for companies: not only security-relevant industries such as defense or semiconductors are affected, but also civilian economic actors. Anyone dependent on critical commodities must increasingly weigh security of supply against protecting their own technologies and trade secrets.

The logic of markets is therefore shifting fundamentally. It is not new measures that create uncertainty—but the consistent application of existing controls and the increasing linkage between access to commodities and information requirements.

China is thus demonstrating that it does not need any further interventions to influence supply, demand, and technological value creation. Control over refining, export processes, and end use is sufficient to steer global supply chains effectively.

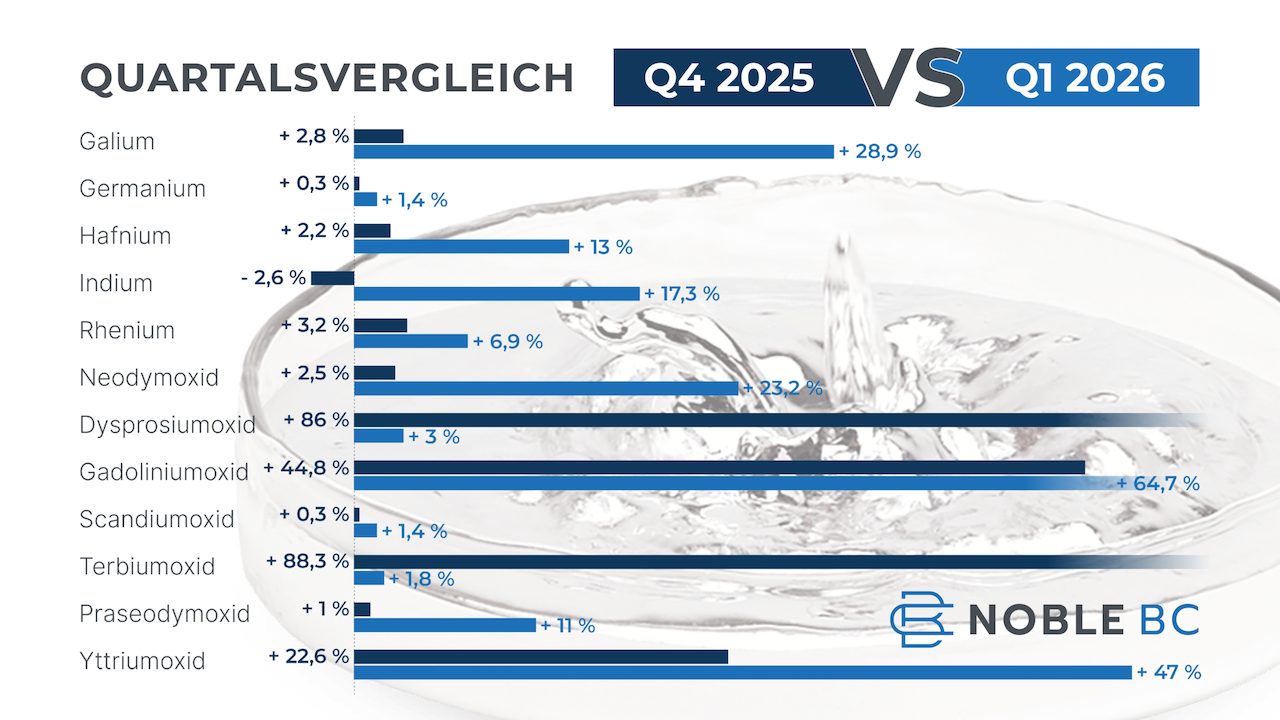

Instead of issuing new export controls, China is introducing state-managed price indices for rare earths such as neodymium oxide and praseodymium oxide. You can read here what is new about this formalization of price formation.

Geopolitical developments are increasingly reflected in concrete projects. Building new mining and processing structures is becoming the key lever to reduce dependencies.

Mining projects

The expansion of new raw material projects is gaining momentum worldwide—but remains significantly behind political targets. While some players are successfully expanding extraction and processing, many projects show a growing gap between strategic ambition and actual implementation.

New alliances and government support programs are intended to close this gap. Yet even politically prioritized projects continue to struggle with permitting, financing, and technical complexity.

The result is a contradictory picture: progress is made where industrial demand, capital, and political support come together. In many cases, however, the transition from planning to production is delayed—and with it the build-up of independent supply chains.

Status of selected raw material projects (Q1 2026)

- ? Lynas (Australia / Malaysia) – functioning supply chain outside China

→ Expansion of extraction and processing, incl. capacities for heavy rare earths - ? Norra Kärr (Sweden) – strategically important, but uncertain

→ Progress in the permitting process, but technical and regulatory hurdles - ? Arafura (Australia) – delays despite priority

→ Final investment decision (FID) postponed again

Assessment of the key projects

Lynas plays a central role in the Western raw materials strategy. As one of the few producers outside China, the company covers not only extraction but increasingly processing as well. With support from the United States, additional capacities are currently being built, including for heavy rare earths—an important step toward reducing dependence on China.

Norra Kärr is one of the most important rare earth projects within Europe—particularly due to its deposits of heavy rare earths such as dysprosium and terbium. At the same time, the project highlights the site’s structural challenges: the commodities are bound in eudialyte, whose processing is technically demanding and so far has only been tested economically to a limited extent. In addition, lengthy permitting procedures and political resistance are delaying implementation. Norra Kärr thus exemplifies the European situation: strategically relevant deposits exist—but their economic utilization remains uncertain.

Arafura illustrates the structural difficulties even for prioritized projects. The Nolans project has been under development for around two decades and has already received substantial public funding. Nevertheless, the final investment decision has been postponed multiple times—most recently to the first half of 2026. This shows that even strategically central projects remain dependent on financing and execution risks.

Recycling – the fast lever

While new mining projects take years to decades, part of the solution is already emerging within existing industrial processes.

An example from European industry shows the potential here:

In the production of battery cells, the BMW Group relies on mechanical direct recycling—not only at the end of a product’s life, but already during production. Production scrap and unused battery cells are mechanically dismantled, sorted, and fed directly back into manufacturing—without energy-intensive chemical processes and without detours via third countries.

The effect goes far beyond efficiency:

Valuable materials remain in the loop, demand for primary raw materials declines, supply chains become shorter and more predictable—and dependence on external actors is measurably reduced.

Recycling is thus developing into a strategic instrument for securing raw materials. Not as a replacement for new projects—but as one of the few levers that can have an impact in the short term.

This approach is gaining importance especially in Europe: while mining projects often fail due to permitting, financing, or infrastructure, recycling can be integrated directly into existing industrial processes.

Independence therefore begins not only in mining—but in production itself.

Technology & demand

Innovation spotlights

Technological breakthroughs are increasingly changing demand for critical raw materials. New applications do not emerge in isolation, but are based on highly specialized materials used in ever more complex systems. Especially in the areas of energy, robotics, and semiconductors, it is clear how closely innovation and raw material demand are linked.

Wireless power transmission

New research in quantum materials shows that, in the future, energy may no longer necessarily need to be transmitted via physical lines. Initial prototypes enable power transmission via light and could fundamentally change the concept of energy storage.

- Use of indium in photonic and quantum-based systems

Flexible drives using liquid metals

A new approach in drive technology uses liquid gallium instead of rigid mechanical components. Electric fields set the metal in motion, enabling flexible, compact drive systems.

- Key technology for soft robotics, medical technology, and miniaturization

Efficiency leap in photovoltaics

Modern tandem solar cells combine multiple semiconductor layers to efficiently utilize different spectral ranges of light. Efficiencies of over 34% demonstrate the potential of this technology.

- Use of germanium, gallium, and indium in high-performance cells

Growth Markets

Rising demand for critical raw materials is increasingly being driven by structural growth markets. Unlike short-term demand spikes, these developments are based on long-term technological trends that generate stable demand over many years.

This is particularly evident in two areas: the global space industry and the energy transition. Both sectors grow independently of economic cycles and require a wide range of specialized metals that can only be substituted to a limited extent.

In satellite technology, the growing importance of communications, Earth observation, and security-relevant applications is driving continuous expansion of infrastructure in orbit. At the same time, the global expansion of renewable energy—especially photovoltaics—continues to increase demand for high-performance materials.

What these markets have in common is that they are not only growing, but also increasing technological complexity. This also increases dependence on critical raw materials along the entire value chain.

CAGR forecast (satellites & solar)

- Satellite propulsion systems:

- Market size from $11.05 bn (2024) to $23.24 bn (2030)

- CAGR: 13.6% (2025–2030)

- Photovoltaics (global):

- Installed capacity from approx. 1.6 TW (2023) to over 5 TW (2030)

- CAGR: ~18% (2023–2030)

- Annual additions grow to >500 GW

- Rising demand for gallium, germanium, and indium

Conclusion: Access is decisive

The first quarter of 2026 marks a clear turning point: commodities are no longer a classic market, but a strategic instrument of geopolitical power.

Developments in recent months show how closely access to commodities, technological development, and security-policy interests are linked. States are building strategic reserves, deliberately securing supply chains, and increasingly shifting economic decisions into the geopolitical arena.

At the same time, structural demand continues to rise due to new technologies. Innovation, the energy transition, and digitalization increase dependence on precisely those materials whose supply can be politically controlled.

This fundamentally changes the logic of markets:

Competitiveness is no longer determined by price—but by secure access.

For Europe, this results in a dual challenge. Alongside expanding military capabilities, securing raw material supply chains becomes a prerequisite for industrial and strategic capacity to act. New partnerships, in-house projects, and technological capabilities along the value chain are decisive.

Commodities are increasingly becoming a geopolitical hedge in a world of growing uncertainty.

Access is power.

Recommendations for action 2026+

- ? Secure access strategically—not just purchase

- Long-term partnerships, direct investments, and secured supply contracts are gaining importance

- ? Think supply chains holistically

- What matters is not only access to raw materials, but control over processing (midstream), application (endstream), and know-how

- ? Integrate recycling systematically

- Use secondary raw materials as a lever with short-term impact to reduce external dependencies

- ? Actively drive diversification

- Build alternative sources of supply outside China—even at higher costs

- ? Concentration in refining remains the biggest risk

- Key processing steps remain heavily concentrated in China

Strategic implementation: making commodities investable

While states build strategic reserves and companies secure their supply chains, new approaches are also emerging in capital markets to enable access to critical commodities.

Seltene Erden AG is pursuing the goal of selectively acquiring production-critical metals and building a strategic reserve in Germany. The holdings are stored physically, fully insured, and their warehousing is documented transparently and tamper-proof on a public blockchain.

This creates, for the first time, the opportunity to participate directly in the development of strategic commodities via traditional capital market instruments—while also contributing to security of supply in Europe.

The approach shows that commodities are no longer just an issue for industry and politics—they are increasingly developing into an independent asset class with strategic significance.

Expert commentary

Commodities are no longer a commodity—they are strategy

Andreas Kroll

The world is electrified—and commodity markets react immediately. Conflicts in the Middle East, tensions around Venezuela, and an increasingly unstable geopolitical situation are driving energy and metal prices higher. But anyone who believes this is already the peak underestimates the momentum. Because even Charles-Edouard Bilbault of Rothschild & Co Asset Management emphasizes: we are only at the beginning of a new commodity cycle.

This is being driven by three structural forces:

First, the energy transition—electric vehicles, grid expansion, and renewable energy multiply metal demand.

Second, new technologies—data centers, AI, and electrification continue to push demand higher.

And third, deglobalization—supply chains are being viewed politically, no longer only economically.

This inevitably turns attention to China.

Because the real power lies not in access to commodities—but in their processing. And that is precisely where China has built a dominant position over decades. More than half of global refining, and for critical materials in some cases up to 80%, is in Chinese hands.

A complete export stop for rare earths would hit the West’s industrial base within a very short time. No chips, no high technology, no modern defense systems.

China has thus effectively become the decisive actor in the global commodities system.

Europe, by contrast, is lagging behind.

Not because there are no resources—but because the industrial infrastructure is missing.

And at the same time, the most important partner is becoming more unpredictable.

The United States under Trump is acting increasingly unilaterally, making decisions on its own and then expecting unity afterward. For Europe, this means: we must broaden our base and build new partnerships.

Industry has long recognized this reality.

At the latest since last year’s export controls, it has been clear: “just in time” no longer works. Companies are no longer looking for the best price—they are looking for security of supply.

Against this backdrop, new models are emerging.

Noble Elements has, for the first time, begun to lend physical commodities specifically to industry. The aim is to bridge short-term bottlenecks and restore companies’ ability to act.

But individual initiatives are not enough.

At the political level, there are initial approaches in the right direction—such as the Critical Raw Materials Act or “Readiness 2030”.

What is missing, however, is a consistently implemented, coordinated commodities strategy.

What must happen now:

- Bundling industrial demand → Only large offtake volumes create negotiating power

- Minimum prices and government planning certainty → Not to distort the market, but as a basis for investment

- Diversification quotas outside China → Implement consistently, following the example of other industrial nations

- More speed in international partnerships → Projects in Africa, Australia, or Central Asia are being decided now—not in five years, because in the end it is about more than commodities.

Because in the end it is about more than commodities.

Without secure, diversified supply chains, Europe will lose not only materials—but industrial value creation, jobs, and technological sovereignty.